Options, Futures And Other Derivatives By John C. Hull + Cd

Lo que tienes que saber de este producto

- Género: Ciencias económicas.

- Administración.

- Edad recomendada: de a .

- ISBN: 9780273759072.

Características del producto

Características principales

Autor | John C. Hull |

|---|---|

Idioma | Inglés |

Editorial del libro | Pearson |

Año de publicación | 2012 |

Otros

Género del libro | Ciencias económicas |

|---|---|

Tipo de narración | Administración |

Descripción

Soft cover

848 p.

For undergraduate and graduate courses in derivatives, options and futures, financial engineering, financial mathematics, and risk management.

Bridge the gap between theory and practice.

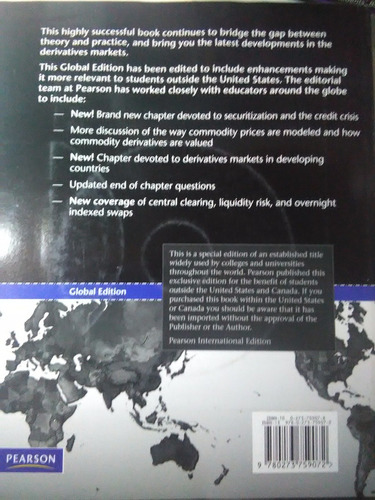

Designed to bridge the gap between theory and practice, this introductory text on the futures and options markets is ideal for those with a limited background in mathematics.

The eighth edition has been updated and improved—featuring a new chapter on securitization and the credit crisis, and increased discussion on the way commodity prices are modeled and commodity derivatives valued.

Provide the right balance: Mathematical Sophistication. In the study of derivatives, if the level of mathematical sophistication is too high, then the material is likely to be inaccessible to many students and practitioners. But if it’s too low, then some important issues may not get the in-depth explanation they need. To help, this text takes a balanced approach to mathematical sophistication by:

Eliminating nonessential mathematical material or including it in the end-of-chapter appendices and/or technical notes on the website.

Providing a careful explanation of the concepts that are likely to be new to many readers—along with presenting the concepts with many numerical examples.

Updated! Offer the latest software: DerivaGem version 2.00 is included with this book. There is a new Getting Started section at the end of the book—and DerivaGem is now compatible with Office, Mac, and Linux users. This program consists of two Excel applications:

The Options Calculator consists of easy-to-use software for valuing a wide range of options.

The Applications Builder consists of a number of Excel functions from which users can build their own applications. It includes a number of sample applications and enables students to explore the properties of options and numerical procedures more easily. It also allows more interesting assignments to be designed.

NEW! Cover the credit crisis: New Chapter 8. The new Chapter 8: Securitization and the Credit Crisis of 2007 is entirely devoted to securitization and the credit crisis. The events in the financial markets since the last edition made this update necessary and particularly relevant.

Updated! Present relevant material:

Chapter 33 now includes increased discussion on the way commodity prices are modeled and commodity derivatives valued.

Chapter 3 has been simplified and contains an appendix explaining the capital asset pricing model.

Chapter 12 contains a new appendix to show that the Black-Scholes-Merton formula can be derived as the limiting case of a binomial tree.

New to This Edition

Updated! Offer the latest software: DerivaGem version 2.00 is included with this book. There is a new Getting Started section at the end of the book—and DerivaGem is now compatible with Office, Mac, and Linux users. This program consists of two Excel applications:

The Options Calculator consists of easy-to-use software for valuing a wide range of options.

The Applications Builder consists of a number of Excel functions from which users can build their own applications. It includes a number of sample applications and enables students to explore the properties of options and numerical procedures more easily. It also allows more interesting assignments to be designed.

NEW! Cover the credit crisis: New Chapter 8. The new Chapter 8: Securitization and the Credit Crisis of 2007 is entirely devoted to securitization and the credit crisis. The events in the financial markets since the last edition made this update necessary and particularly relevant.

Updated! Present relevant material:

Chapter 33 now includes increased discussion on the way commodity prices are modeled and commodity derivatives valued.

Chapter 3 has been simplified and contains an appendix explaining the capital asset pricing model.

Chapter 12 contains a new appendix to show that the Black-Scholes-Merton formula can be derived as the limiting case of a binomial tree.

Table of Contents

Chapter 1. Introduction

Chapter 2. Mechanics of Futures Markets

Chapter 3. Hedging Strategies Using Futures

Chapter 4. Interest Rates

Chapter 5. Determination of Forward and Futures Prices

Chapter 6. Interest Rate Futures

Chapter 7. Swaps

Chapter 8. Securitization and the Credit Crisis of 2007

Chapter 9. Mechanics of Options Markets

Chapter 10. Properties of Stock Options

Chapter 11. Trading Strategies Involving Options

Chapter 12. Binomial Trees

Chapter 13. Wiener Processes and Ito’s Lemma

Chapter 14. The Black-Scholes-Merton Model

Chapter 15. Employee Stock Options

Chapter 16. Options on Stock Indices and Currencies

Chapter 17. Options on Futures

Chapter 18. Greek Letters

Chapter 19. Volatility Smiles

Chapter 20. Basic Numerical Procedures

Chapter 21. Value at Risk

Chapter 22. Estimating Volatilities and Correlations

Chapter 23. Credit Risk

Chapter 24. Credit Derivatives

Chapter 25. Exotic Options

Chapter 26. More on Models and Numerical Procedures

Chapter 27. Martingales and Measures

Chapter 28. Interest Rate Derivatives: The Standard Market Models

Chapter 29. Convexity, Timing, and Quanto Adjustments

Chapter 30. Interest Rate Derivatives: Models of the Short Rate

Chapter 31. Interest Rate Derivatives: HJM and LMM

Chapter 32. Swaps Revisited

Chapter 33. Energy and Commodity Derivatives

Chapter 34. Real Options

Chapter 35. Derivatives Mishaps and What We Can Learn from Them

En la compra de dos libros de igual o diferente precio de cualquiera de nuestras publicaciones podrá escoger un tercer libro gratis.

Haga usted sus preguntas sobre esta promoción antes de comprar.

El cual deberá ser del mismo precio que el de menor costo mismo que se le enviara en el mismo paquete .

En el momento de hacer la compra deberá ponerse en contacto con nosotros para dar su elección y poder enviárselo ya que no podría enviarse después